![[warehouse+district+brochure+pg+1.jpg]](https://blogger.googleusercontent.com/img/b/R29vZ2xl/AVvXsEiwgbfkUPI5trRPMl1NR4IyCzeFiomxfdNQ80TtUoQtd59vqJn_my2joBVg4W5N-QmIAq6zAlyAGfFFQVnb-ekb2BRVe3DJxFHP9TdpH82d-9YjEz346wEyHBcrzgDGDxrdXJ5vqSc65eM/s1600/warehouse+district+brochure+pg+1.jpg)

![[warehouse+district+brochure+pg+2.jpg]](https://blogger.googleusercontent.com/img/b/R29vZ2xl/AVvXsEiqYp2tS9qPbxLAkqU1k8FPAyhkYjyTmBijaLC_YzoJSmiCZxRl3fiv_SVPTlaAOFAXK5u_ezkq5cLKxU6f1Y5ozg2wx7qKtkruMBzKoHnL1Y27mnHWxba3IPEz2TZWsPPYnYRwb7o1UnE/s1600/warehouse+district+brochure+pg+2.jpg)

![[Big_BUild_07-14-08.jpg]](https://blogger.googleusercontent.com/img/b/R29vZ2xl/AVvXsEh1dPqaQx67XDlM2V21nTCuxdaeIl6-9J9IjmmGQe64PM9eBpegJbzLhsa0vbpEsRemd3tFQ1tBvMwfOMlSC9xwh6_PebM7zQgXw1rtoVsOeej2x5VUwsRZSEUnYey6V5H3aSq7B8OmlH4/s1600/Big_BUild_07-14-08.jpg)

Warehouse Brochure Map Updated

--

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

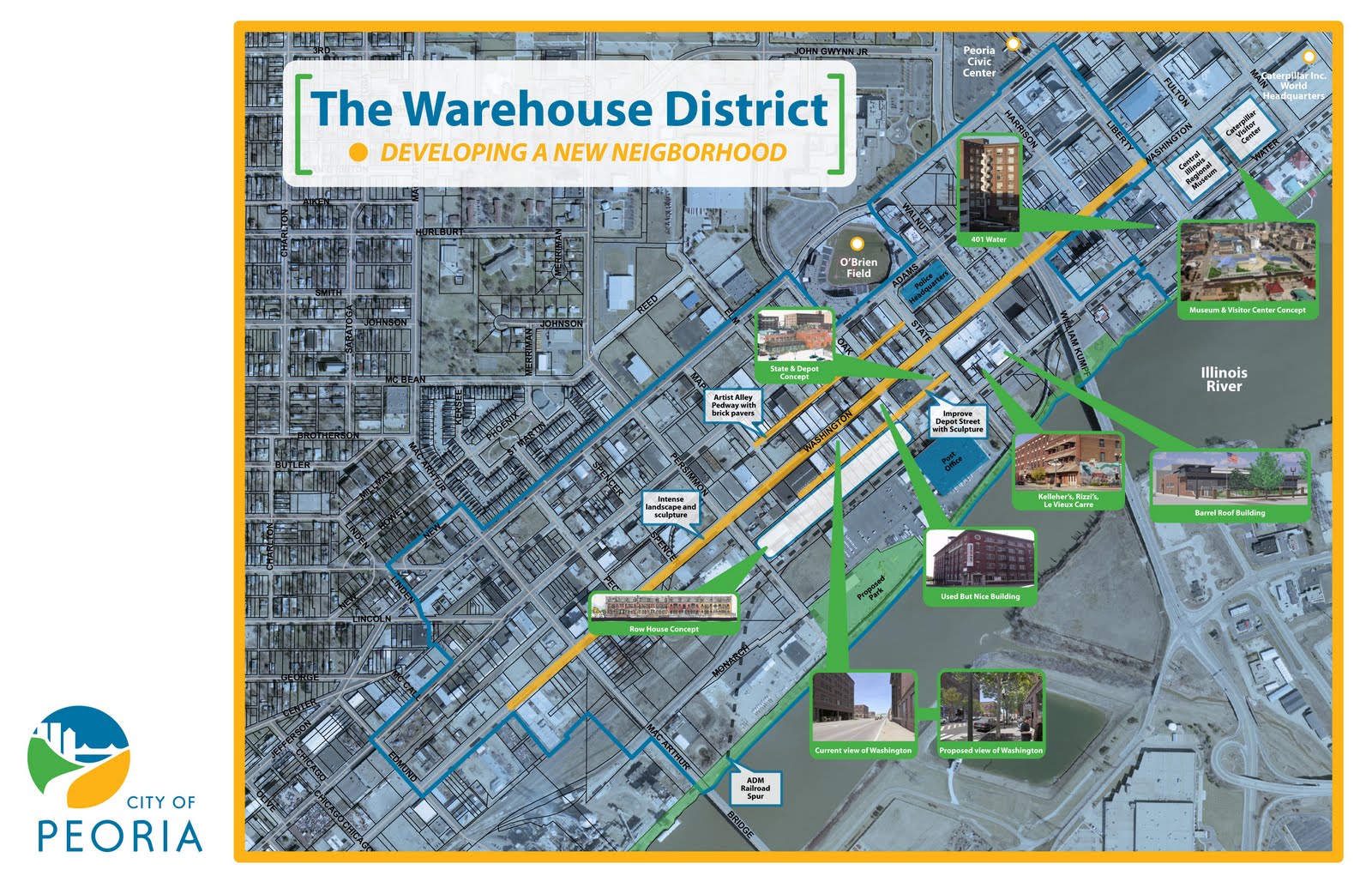

Warehouse Brochure Map Updated. Click to make it larger.

-

Your update suggestions or corrections will be appreciated.

-

Send them to Craighullinger@gmail.com

-

Your update suggestions or corrections will be appreciated.

-

Send them to Craighullinger@gmail.com

-

--

CONGRATULATIONS TO THE DEVELOPERS OF THE SEALTEST BUILDING

-

CONGRATULATIONS TO THE DEVELOPERS OF THE SEALTEST BUILDING

-

City Council approved this great redevelopment unanimously 9-0.-This is the 16th building approved for redevelopment or development with the last three years in the Tax Increment Financing (TIF) Districts - this during the Great Recession.

-

Click on the links below for more info:

-

http://warehousedistrict.blogspot.com/2009/09/sealtest-building-latest-warehouse.html

-

http://warehousedistrict.blogspot.com/

-

-

Click on the links below for more info:

-

http://warehousedistrict.blogspot.com/2009/09/sealtest-building-latest-warehouse.html

-

http://warehousedistrict.blogspot.com/

-

-

Proposed Historic Preservation Tax Credit Act

Federal Historic Tax Credits are a major incentive that helps older cities renew declining neighborhoods. The tax credit makes the preservation and renewal of older buildings much more likely, and is an important factor in revializing older neighborhoods. A number of States have similar programs.

The following draft act is based on the successful acts used in the State of Kansas and Missouri. If Illinois passed a similar act, we anticipate a substantial increase in redevelopment of older neighborhoods. The passage of an act like this would greatly help the redevelopment of older neighborhoods such as Renaissance Park and the Warehouse District.

This Act may be cited as the Illinois Historic Preservation Tax Credit Act.Sec. 2. Definitions, As used in this section, unless the context clearly indicates otherwise:

(a) "Qualified expenditures" means all the costs and expenses of exterior and interior rehabilitation and construction, including all costs relating to adaptive reuse and parking structures therefor, incurred by a qualified taxpayer in the restoration and preservation of a qualified historic structure pursuant to a qualified rehabilitation plan;

(b) "qualified historic structure" means any building, regardless of whether said building is income producing, is a condominium building or is of any other ownership structure, which is defined as a certified historic structure by section 47 (c)(3) of the federal internal revenue code, is individually listed on the register of Illinois historic places, or is located and contributes to a district listed on the register of Illinois historic places, or is located and contributes to a district listed on the register of Illinois Main Street places, or is located and contributes to a district listed on a local register of historic places within a home rule county or home rule municipality;

(c) "qualified rehabilitation plan" means a project which is approved by the Illinois Historic Preservation Agency, or by a local historic preservation commission certified by the Illinois Historic Preservation Agency to so approve according to rules and regulations adopted by the agency, or by a local historic preservation commission of a home rule county or home rule municipality, as being consistent with the standards for rehabilitation and guidelines for rehabilitation of historic buildings as adopted by the federal secretary of interior and in effect on the effective date of this act; and4

(d) "qualified taxpayer" means the owner of the qualified historic structure or any other person who may qualify for the federal rehabilitation credit allowed by section 47 of the federal internal revenue code. If the taxpayer is a corporation having an election in effect under subchapter S of the federal internal revenue code, a partnership or a limited liability company, the credit provided by this subsection shall be claimed by the shareholders of such corporation, the partners of such partnership or the members of such limited liability company in the same manner as such shareholders, partners or members account for their proportionate shares of the income or loss of the corporation, partnership or limited liability company, or as the corporation, partnership or limited liability company mutually agree as provided in the bylaws or other executed agreement. Credits granted to a partnership, a limited liability company taxed as a partnership or other multiple owners of property shall be passed through to the partners, members or owners respectively pro rata or pursuant to an executed agreement among the partners, members or owners documenting any alternate distribution method.

-Sec. 3. Allowable Credit. For all taxable years commencing after December 31, 2007, there shall be allowed a tax credit against the income or any other tax liability imposed upon a taxpayer pursuant to the 35 ILCS, except any tax liability imposed by 35 ILCS 130/ through 35 ILCS 143/ and 35 ILCS 200/, in an amount equal to 25% of qualified expenditures incurred in the restoration and preservation of a qualified historic structure pursuant to a qualified rehabilitation plan by a qualified taxpayer if the total amount of such expenditures equal $5,000 or more. If the amount of such tax credit exceeds the qualified taxpayer's income or other qualifying tax liability for the year in which the qualified rehabilitation plan was placed in service, such excess amount may be carried over for deduction from such taxpayer's income or other qualifying tax liability in the next succeeding year or years until the total amount of the credit has been deducted from tax liability, except that no such credit shall be carried over for deduction after the 10th taxable year succeeding the taxable year in which the qualified rehabilitation plan was placed in service.

Sec. 4. Transfer of Credits. Any person, hereinafter designated the assignor, may sell, assign, convey or otherwise transfer tax credits allowed and earned pursuant to section 3. The taxpayer acquiring credits, hereinafter designated the assignee, may use the amount of the acquired credits to offset up to 100% of its income or other qualifying tax liability for either the taxable year in which the qualified rehabilitation plan was first placed into service or the taxable year in which such acquisition was made. Unused credit amounts claimed by the assignee may be carried forward for up to 10 years or backward for up to 3 years, except that all such amounts shall be claimed within 10 years following the tax year in which the qualified rehabilitation plan was first placed into service. The assignor shall enter into a written agreement with the assignee establishing the terms and conditions of the agreement and shall perfect such transfer by notifying the Illinois Historic Preservation Agency in writing within 90 calendar days following the effective date of the transfer and shall provide any information as may be required by such agency to administer and carry out the provisions of this section. The amount received by the assignor of such tax credit shall be taxable as capital gains income of the assignor, and the excess of the value of such credit over the amount paid by the assignee for such credit shall be taxable as capital gains income of the assignee.

Sec. 5. Annual County Limit. The cumulative amount allowable for such credits shall be limited to a maximum of $25 million per year per county. Notwithstanding the 10-year deduction period for such credits, in the event a credit is disallowed because it exceeds the annual $425 million cumulative limit per county, said credit shall be allowed the next year if within said limit or the claim period for such credit shall be extended by one additional year for each year disallowed as a result of this section. Except in cases of bad faith or fraud, no penalty or interest shall be due as a result of any credit disallowed by this section.

Sec. 6. Biennial Report. The Department of Commerce and Economic Opportunity shall determine, on a biennial basis beginning at the end of the second fiscal year after the date this Act takes effect, the overall economic impact to the state from the rehabilitation of eligible property.

The following draft act is based on the successful acts used in the State of Kansas and Missouri. If Illinois passed a similar act, we anticipate a substantial increase in redevelopment of older neighborhoods. The passage of an act like this would greatly help the redevelopment of older neighborhoods such as Renaissance Park and the Warehouse District.

------------------

Proposed 35 ILCS 12/Illinois Historic Preservation Tax Credit Act

Credit Against Tax For Certain Historic Structure Rehabilitation Expenditures.Sec. 1. Short Title.

This Act may be cited as the Illinois Historic Preservation Tax Credit Act.Sec. 2. Definitions, As used in this section, unless the context clearly indicates otherwise:

(a) "Qualified expenditures" means all the costs and expenses of exterior and interior rehabilitation and construction, including all costs relating to adaptive reuse and parking structures therefor, incurred by a qualified taxpayer in the restoration and preservation of a qualified historic structure pursuant to a qualified rehabilitation plan;

(b) "qualified historic structure" means any building, regardless of whether said building is income producing, is a condominium building or is of any other ownership structure, which is defined as a certified historic structure by section 47 (c)(3) of the federal internal revenue code, is individually listed on the register of Illinois historic places, or is located and contributes to a district listed on the register of Illinois historic places, or is located and contributes to a district listed on the register of Illinois Main Street places, or is located and contributes to a district listed on a local register of historic places within a home rule county or home rule municipality;

(c) "qualified rehabilitation plan" means a project which is approved by the Illinois Historic Preservation Agency, or by a local historic preservation commission certified by the Illinois Historic Preservation Agency to so approve according to rules and regulations adopted by the agency, or by a local historic preservation commission of a home rule county or home rule municipality, as being consistent with the standards for rehabilitation and guidelines for rehabilitation of historic buildings as adopted by the federal secretary of interior and in effect on the effective date of this act; and4

(d) "qualified taxpayer" means the owner of the qualified historic structure or any other person who may qualify for the federal rehabilitation credit allowed by section 47 of the federal internal revenue code. If the taxpayer is a corporation having an election in effect under subchapter S of the federal internal revenue code, a partnership or a limited liability company, the credit provided by this subsection shall be claimed by the shareholders of such corporation, the partners of such partnership or the members of such limited liability company in the same manner as such shareholders, partners or members account for their proportionate shares of the income or loss of the corporation, partnership or limited liability company, or as the corporation, partnership or limited liability company mutually agree as provided in the bylaws or other executed agreement. Credits granted to a partnership, a limited liability company taxed as a partnership or other multiple owners of property shall be passed through to the partners, members or owners respectively pro rata or pursuant to an executed agreement among the partners, members or owners documenting any alternate distribution method.

-Sec. 3. Allowable Credit. For all taxable years commencing after December 31, 2007, there shall be allowed a tax credit against the income or any other tax liability imposed upon a taxpayer pursuant to the 35 ILCS, except any tax liability imposed by 35 ILCS 130/ through 35 ILCS 143/ and 35 ILCS 200/, in an amount equal to 25% of qualified expenditures incurred in the restoration and preservation of a qualified historic structure pursuant to a qualified rehabilitation plan by a qualified taxpayer if the total amount of such expenditures equal $5,000 or more. If the amount of such tax credit exceeds the qualified taxpayer's income or other qualifying tax liability for the year in which the qualified rehabilitation plan was placed in service, such excess amount may be carried over for deduction from such taxpayer's income or other qualifying tax liability in the next succeeding year or years until the total amount of the credit has been deducted from tax liability, except that no such credit shall be carried over for deduction after the 10th taxable year succeeding the taxable year in which the qualified rehabilitation plan was placed in service.

Sec. 4. Transfer of Credits. Any person, hereinafter designated the assignor, may sell, assign, convey or otherwise transfer tax credits allowed and earned pursuant to section 3. The taxpayer acquiring credits, hereinafter designated the assignee, may use the amount of the acquired credits to offset up to 100% of its income or other qualifying tax liability for either the taxable year in which the qualified rehabilitation plan was first placed into service or the taxable year in which such acquisition was made. Unused credit amounts claimed by the assignee may be carried forward for up to 10 years or backward for up to 3 years, except that all such amounts shall be claimed within 10 years following the tax year in which the qualified rehabilitation plan was first placed into service. The assignor shall enter into a written agreement with the assignee establishing the terms and conditions of the agreement and shall perfect such transfer by notifying the Illinois Historic Preservation Agency in writing within 90 calendar days following the effective date of the transfer and shall provide any information as may be required by such agency to administer and carry out the provisions of this section. The amount received by the assignor of such tax credit shall be taxable as capital gains income of the assignor, and the excess of the value of such credit over the amount paid by the assignee for such credit shall be taxable as capital gains income of the assignee.

Sec. 5. Annual County Limit. The cumulative amount allowable for such credits shall be limited to a maximum of $25 million per year per county. Notwithstanding the 10-year deduction period for such credits, in the event a credit is disallowed because it exceeds the annual $425 million cumulative limit per county, said credit shall be allowed the next year if within said limit or the claim period for such credit shall be extended by one additional year for each year disallowed as a result of this section. Except in cases of bad faith or fraud, no penalty or interest shall be due as a result of any credit disallowed by this section.

Sec. 6. Biennial Report. The Department of Commerce and Economic Opportunity shall determine, on a biennial basis beginning at the end of the second fiscal year after the date this Act takes effect, the overall economic impact to the state from the rehabilitation of eligible property.

More info:

http://cityofpeoria.blogspot.com/2009/05/proposed-illinois-historic-preservation.html

http://www.illinoishistory.gov/ps/index.htm

http://cityofpeoria.blogspot.com

http://cityofpeoria.blogspot.com/2009/05/proposed-illinois-historic-preservation.html

http://www.illinoishistory.gov/ps/index.htm

http://cityofpeoria.blogspot.com

Four Buildings Proposed for Redevelopment

On Tuesday September 22, 2009 City Council will consider proposed redevelopment agreements for four buildings. The first three buildings face Washington Street. The drawing above shows the three buildings from the perspective of the alley between 401 Water Street and Washington Street. The buildings will be interconnected.

The other building under consideration is the Edgewater Building facing the Illinois River and 401 Water Street.

The four buildings total 66,800 square feet. Costs are estimated at $6,790,000.

These great redevelopments will help continue the ongoing efforts to revitalize and renew the Heart of Peoria. They will bring jobs and vitality to the area.

Agenda Date Requested: September 22, 2009

Agenda Date Requested: September 22, 2009

Action Requested: APPROVAL TO ENTER INTO A TIF REDEVELOPMENT AGREEMENT WITH HGI, L.L.C. AND AUTHORIZE THE INTERIM CITY MANAGER TO EXECUTE THE NECESSARY DOCUMENTS. THIS PROJECT IS LOCATED IN THE CENTRAL BUSINESS DISTRICT TIF. (COUNCIL DISTRICT 1)

Background: The Redeveloper plans to completely reconstruct three adjacent properties:

408 SW Washington Street is a four story 24,000 square foot former retail store and warehouse. The property will be reconstructed into a first class office building. Renovations to include but not limited to a complete reconstruction and bringing the building into compliance with governing body codes for accessibility, fire and structural safety.

Estimated cost for complete renovations of this building are $1,800,000.00

412 SW Washington Street is one story 12,000 square foot former assembly, printing and warehouse building. The property will be reconstructed into a first class office building. Renovations to include but not limited to a complete reconstruction and bringing the building into compliance with governing body codes for accessibility, fire and structural safety.

Estimated cost for complete renovations of this building are $1,600,000.00

420 SW Washington Street will be a new 10,800 square foot building inside the existing façade of a former retail store and warehouse building. The property will be reconstructed into a first class office building. Renovations to include but not limited to a complete construction and bringing the building into compliance with governing body codes for accessibility, fire and structural safety.

Estimated cost for complete renovations of this building are $1,800,000.00

412 SW Washington Street is one story 12,000 square foot former assembly, printing and warehouse building. The property will be reconstructed into a first class office building. Renovations to include but not limited to a complete reconstruction and bringing the building into compliance with governing body codes for accessibility, fire and structural safety.

Estimated cost for complete renovations of this building are $1,600,000.00

420 SW Washington Street will be a new 10,800 square foot building inside the existing façade of a former retail store and warehouse building. The property will be reconstructed into a first class office building. Renovations to include but not limited to a complete construction and bringing the building into compliance with governing body codes for accessibility, fire and structural safety.

Estimated cost for complete renovations of this building are $1,140,000.00

Financial Impact: HGI, L.L.C. is asking for a TIF Redevelopment Agreement with a 50/50 split of the property tax for the life of the TIF. Conservative estimates indicate property tax on the increment would result in a total of $979,480 over the life of the TIF with $489,740 going to the City for infrastructure improvements (Exhibit A). The property is located in the Enterprise zone and the company is eligible to receive the sales tax exemption on building materials that is estimated to be $181,600; the City’s portion being $56,750.

NEIGHBORHOOD CONCERNS: There are no neighborhood concerns.

Impact if Approved: The City will enter into a redevelopment agreement with HGI, L.L.C. which will provide them with an incentive to redevelop and renovate the property. The redeveloper will receive 50% of the property tax increment over the life of the TIF and the City will capture the remaining 50% of the property tax increment to utilize for infrastructure improvements.

Impact if Denied: The City will not enter into the redevelopment agreement and the City will not capture the property tax for infrastructure improvements.

Alternatives1: None

EEO Certification Number: In Process

RELATIONSHIP TO THE COMPREHENSIVE PLAN: This project assists in achieving both the vision and goals of the Comprehensive Plan as follows:

Chapter 5 ECONOMICS--VISION: A HEALTHY, THRIVING ECONOMY; and GOAL: A.1. Provide an economic environment that supports existing and new businesses. A1.8. Consider providing public money to encourage private investment.

Agenda Date Requested: September 22, 2009

Action Requested: APPROVAL TO ENTER INTO A TIF REDEVELOPMENT AGREEMENT WITH IRON FRONT, L.L.C. AND AUTHORIZE THE INTERIM CITY MANAGER TO EXECUTE THE NECESSARY DOCUMENTS. THIS PROJECT IS LOCATED IN THE WEARHOUSE DISTRICT TIF. (COUNCIL DISTRICT 1)

Background: The Redeveloper plans to completely reconstruct the Edgewater Building. The structure is a two story 20,000 square foot former parking deck turned warehouse. It will be reconstructed into a first class office building with parking. Renovations to include but not limited to, a complete reconstruction and bringing the building into compliance with governing codes for accessibility, fire and structural safety.

Estimated cost of complete renovation is $2,250,000.

Financial Impact: Iron Front, L.L.C. is asking for a TIF Redevelopment Agreement with a 50/50 split of the property tax for the life of the TIF. Conservative estimates indicate property tax on the increment would result in a total of $882,591 over the life of the TIF with $441,296 going to the City for infrastructure improvements (Exhibit A). The property is located in the Enterprise zone and the company is eligible to receive the sales tax exemption on building materials that is estimated to be $90,000; the City’s portion being $28,125.

NEIGHBORHOOD CONCERNS: There are no neighborhood concerns.

Impact if Approved: The City will enter into a redevelopment agreement with Iron Front, L.L.C. which will provide them with an incentive to redevelop and renovate the property. The redeveloper will receive 50% of the property tax increment over the life of the TIF and the City will capture the remaining 50% of the property tax increment to utilize for infrastructure improvements.

Impact if Denied: The City will not enter into the redevelopment agreement and the City will not capture the property tax for infrastructure improvements.

Alternatives1: None

EEO Certification Number: In Process

RELATIONSHIP TO THE COMPREHENSIVE PLAN: This project assists in achieving both the vision and goals of the Comprehensive Plan as follows:

Chapter 5 ECONOMICS--VISION: A HEALTHY, THRIVING ECONOMY; and GOAL: A.1. Provide an economic environment that supports existing and new businesses. A1.8. Consider providing public money to encourage private investment.

Sealtest Building Latest Warehouse Redevelopment

This building is proposed for mixed use redevelopment, and will be considered by the City Council in October 2009.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

TIF Works - Warehouse District up 11%

The graph and chart below show how effectively the two new Tax Increment Financing Districts (TIF's) have worked. Despite "The Great Recession of 2007-2009", Equalized Assessed Evaluation (EAV) has grown very rapidly in the TIF's, faster then the City as a whole and faster then School District 150. 150 lags the City because it's boundary misses the rapidly developing north side of the City.

We believe these numbers support the continued use of Tax Increment Financing. We want our older neighborhoods to thrive and improve, and TIF is one of the best ways to help that process.

We believe these numbers support the continued use of Tax Increment Financing. We want our older neighborhoods to thrive and improve, and TIF is one of the best ways to help that process.

Subscribe to:

Posts (Atom)